Fiscal Policy and Tax Reform in Nigeria: A Spotlight on the Role of Presidential Fiscal Policy and Tax Reform Committee.

By ATER Solomon Vendaga

When the President said he was going to hit the ground running, he meant it. This can be attested by some of the policies and initiatives he has taken. One of these is the Presidential Fiscal Policy and Tax Reform Committee which this short piece will address.

The tax and fiscal regime in the country has been plagued by factors such as overdependence on oil revenue, fiscal indiscipline, bureaucratic corruption, poor economic choices, low tax revenue generation, multiple taxes, tax evasion, etc. These have been the reasons for gargantuan borrowing in large sums at a scary servicing rate, and poor tax-to-GDP ratio, poor environment for business and economic growth amongst other negative economic trends in the country. The President recognising how important a sound fiscal policy environment and an effective taxation system are for the functioning of the government and the economy had in his wisdom taken a positive and formidable step at the earliest opportunity in his administration to review and reform the fiscal and tax regime in the country by setting up a committee to do that.

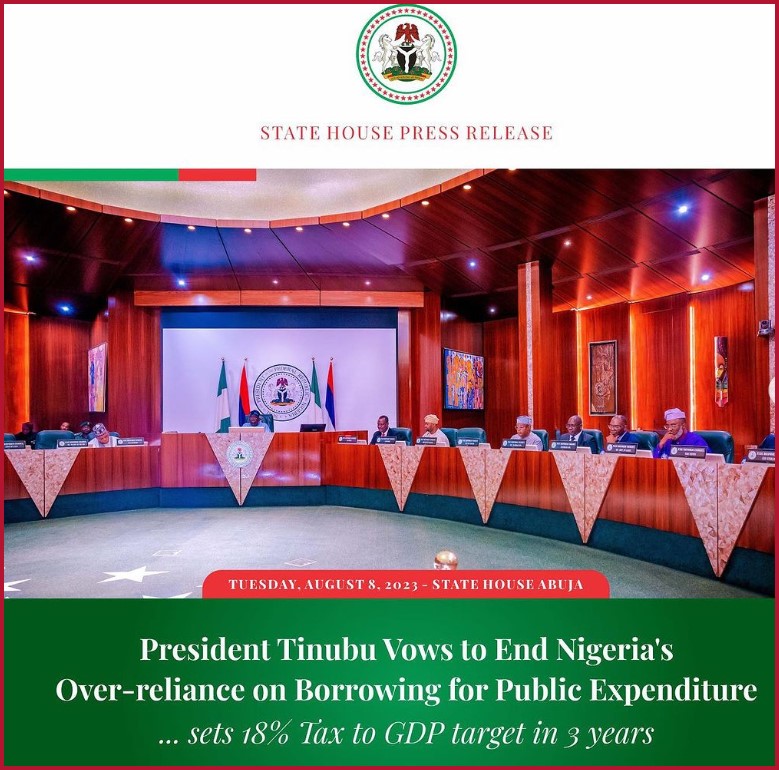

The committee which was inaugurated on the 8th of August, 2023 is headed by an astute and remarkably renowned fiscal and tax policy expert, who is the African Fiscal and Policy Tax Leader at the PricehouseWaterCooper (PwC), Mr Taiwo Oyedele. Its composition cut across diverse MDAs, parastatals, sectors of the economy, expertise and profession numbering about 38 bodies/institutions.

The committee’s work is predicated on three solid pillars;

- Fiscal governance,

- Revenue Transformation and,

- Economic Growth Facilitation and Competitiveness

Each of these pillars bears a close watch. Thus, it is expected that the following will be done:

- Fiscal Governance: The committee’s reforms are expected to give birth to a well coordinated fiscal framework with effective management and oversight of government finances. This involves budgeting, expenditure control, and ensuring transparency and accountability in fiscal operations. Most importantly, to ensure discipline in terms of budgetary allocations, financing, as well as guides on spending choices, etc.

- Revenue Transformation: The Committee’s idea of revenue transformation aims to enhance the government’s income streams sustainably and equitably. It will involve diversifying revenue sources beyond traditional revenue outlets. Tax reforms in this context involve simplifying tax laws, improving tax collection mechanisms, and reducing tax evasion. These reforms can lead to better fiscal discipline and a more stable economic environment.

- Growth Facilitation and Competitiveness: The committee like the President understand that to foster economic growth, tax and fiscal reforms can be designed to incentivize investment and entrepreneurship. This involves reducing tax rates on businesses and providing tax incentives for research and development to encourage young and growing businesses.

Basically, the reform is expected to enhance revenue collection efficiency, ensure transparent reporting, promote the effective utilization of tax and other revenues to boost citizen’s tax morale, and foster a healthy tax culture and drive voluntary compliance.

To achieve the above, the Committee has one (1) year. This shows the urgency of the reform and the weight of importance to quality results it is embedded with.

The one year is further divided into 3 milestones;

- Quick wins which shall run for 30 days. The focus here is to address the issues that do not require critical approaches and can be done easily.

- Critical Tax Reforms which shall run for 6 months. Here the bulk of tax reforms will be carried out. We will see the review of major tax laws, tax policies, harmonization of taxes and revenue collection agencies, effective administration of taxes, adoption of technology, quality of budget and spending transparency, reduction in several taxes, etc.

- Implementation. This will be for 12 months.

Interestingly, the three-mile stones will be run concurrently by the committee’s secretariat.

This committee unlike other committees will be responsible for the implementation of their reforms. This makes sense even more. What is more interesting is that at the end of this reform, the tax-to-GDP ratio is expected to reach 18% in the next 3 years (that is by 2025 or 2026). The current rate to GDP ratio is 10.86% since 2021 which is poor for a country dabbed as the giant of Africa.

Hopes are high that when the committee finishes its work, there will be a thriving environment for economic growth and Competitiveness, increased revenue generation, efficiency of tax collection, transparency and discipline in the fiscal framework, simple and efficient tax and fiscal framework, investor-friendly environment, etc. In fact, fiscal and tax reforms can play a crucial role in shaping a country’s economic landscape. This can help maintain fiscal discipline, increase government revenue, and create a conducive environment for economic growth and competitiveness.

There is no doubt at all as to what this great step taken by the President will achieve given the level of expertise and prowess of the think-tank behind the reform. Nigerians should therefore look forward to a more friendly economy and opportunities for growth and development.

About the Author

Ater, Solomon Vendaga is a final-year law undergraduate at the University of Abuja and the President of the Tax Club University of Abuja and the National Vice President, Association of Nigeria Taxation Students-ANTAS. He can be reached via +2348025263078 or [email protected]

****************************************************************************************

This work is published under the free legal awareness project of Sabi Law Foundation (www.SabiLaw.org) funded by the law firm of Bezaleel Chambers International (www.BezaleelChambers.com). The writer was not paid or charged any publishing fee. You too can support the legal awareness projects and programs of Sabi Law Foundation by donating to us. Donate here and get our unique appreciation certificate or memento.

DISCLAIMER:

This publication is not a piece of legal advice. The opinion expressed in this publication is that of the author(s) and not necessarily the opinion of our organisation, staff and partners.

PROJECTS:

🛒 Take short courses, get samples/precedents and learn your rights at www.SabiLaw.org

🎯 Publish your legal articles for FREE by sending to: [email protected]

🎁 Receive our free Daily Law Tips & other publications via our website and social media accounts or join our free whatsapp group: Daily Law Tips Group 6

KEEP IN TOUCH:

Get updates on all the free legal awareness projects of Sabi Law (#SabiLaw) and its partners, via:

YouTube: SabiLaw

Twitter: @Sabi_Law

Facebook page: SabiLaw

Instagram: @SabiLaw.org_

WhatsApp Group: Free Daily Law Tips Group 6

Telegram Group: Free Daily Law Tips Group

Facebook group: SabiLaw

Email: [email protected]

Website: www.SabiLaw.org

ABOUT US & OUR PARTNERS:

This publication is the initiative of the Sabi Law Foundation (www.SabiLaw.org) funded by the law firm of Bezaleel Chambers International (www.BezaleelChambers.com). Sabi Law Foundation is a Not-For-Profit and Non-Governmental Legal Awareness Organization based in Nigeria. It is the first of its kind and has been promoting free legal awareness since 2010.

DONATION & SPONSORSHIP:

As a registered not-for-profit and non-governmental organisation, Sabi Law Foundation relies on donations and sponsorships to promote free legal awareness across Nigeria and the world. With a vast followership across the globe, your donations will assist us to increase legal awareness, improve access to justice, reduce common legal disputes and crimes in Nigeria. Make your donations to us here or contact us for sponsorship and partnership, via: [email protected] or +234 903 913 1200.

**********************************************************************************