Tax Obligations of NGOs in Nigeria

By ATER, Solomon Vendaga

Introduction

Non-Governmental Organisations (NGOs) exist majorly not for profit making but for the quest to impact society positively. It is for this amongst other reasons that these organizations are regarded as the voice of the common man. Making the space they operate an integral part of our world. In Nigeria, their activities are quite impactful in many areas of our daily lives. It is important to know that these organisations are usually not profit-making entities and because of the nature of their operation, there has been a growing controversy as to their taxable nature. Many people think that since taxes are levied on income/profit made by individuals either juristic or natural and NGOs do not engage in the same gainful ventures, they should not be taxed or not even included in the discussions on taxation. This article is predicated on the need to address the various controversies around the taxation of NGOs in Nigeria and it provides a clear and simple-to-understand piece for those working in the sector.

Definition of an NGO

An NGO is an association of persons registered under Part F of the Companies and Allied Matters Act (CAMA) 2020 as incorporated trustees or Section 26 of CAMA as a company limited by guarantee. An incorporated trustee is to be registered under F of CAMA for the advancement of any religious, educational, literary, scientific, social development, cultural, sporting or charitable purpose. Meanwhile, under S.26 of CAMA, an NGO can be registered as a company limited by guarantee for promoting commerce, art, science, religion, sports, culture, education, research, charity or other similar objects. An NGO incorporated by guarantee is not allowed to carry on business to make profits for distribution to members but be applied solely towards the promotion of its objects.

Taxation and NGOs in Nigeria

It is pertinent to know that before the Finance Act, of 2020, the law required NGOs to file their annual income tax returns in line with Section 55 of the Companies Income Tax Act (CITA) and comply with Value Added Tax (VAT) obligations on the supply or purchase of taxable goods and services. However, the exemption was provided under section 23(1)(c) of the Companies Income Tax Act (“CITA”), section 26(1)(a) of the Capital Gains Tax Act(“CGTA”), and section 19(1) and paragraphs 1 and 13 of the Third Schedule to the Personal Income Tax Act (“PITA”) provide that the profits/income of any institution being a statutory or registered friendly society, company engaged in ecclesiastical, charitable or educational activities of a public character, are exempt from tax, in so far as such profits/income are not derived from a trade or business carried on by such society.

It is important to know that during this time, CITA and other tax laws were not clear on what is meant by “activities of a public character” let alone “public character”. The above lacuna was then the bone of contention about the applicability of income tax to NGOs or its otherwise.

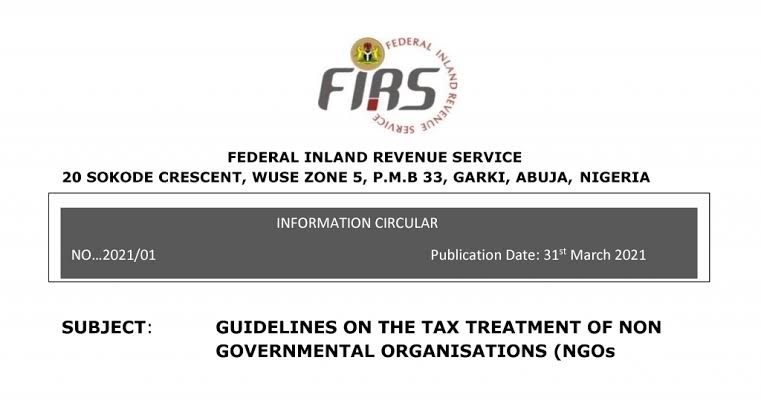

Attempts were taken to address the issue. For instance, the Federal Inland Revenue Service (FIRS) had earlier issued a Circular on 27 August 2010 on the guidelines on the tax exemption status of NGOs. The FIRS in trying to clarify the issue stated that where an NGO engages in any trade or business, the profit derived therefrom will be subjected to income tax as provided by CITA. The Circular further provided that where the NGO invests its assets in any institution, the income derived from such investment shall be subjected to tax and Capital Gains Tax (CGT) shall arise where assets are disposed of by the NGOs at a gain.

The Circular could not fully address the issue as it rather generated more controversies because the law providing for the taxation of companies (where NGOs are registered and operate) did not define keywords necessary for the understanding of their tax obligations. For instance, they argued that in so far as the activities or trade are activities of a public nature and the profit is not distributed among its members, such profit is not taxable and for disposal of assets, they shield themselves under s. 26 of the CGTA.

Consequently, Finance Act defines Public Character to mean an organization or institution is public if it is registered by the relevant law in Nigeria, and does not distribute or share its profits in any manner with its members or promoters. (s. 105 of CITA as amended by s. 21(b) of the Finance Act, 2020. The definition to some extent is brought to still reverse.

In addition to the above, the FIRS, on 31 March 2021, released a Circular on the guidelines on the tax treatment of NGOs and suggests that the income of an NGO is to be wholly used for the objectives of the organization or institution and shall be for the interest of the public. The Circular further states that the distribution of assets, whether in cash or in-kind (e.g. gifting a vehicle or any asset for the personal use of the promoters or members) shall be construed as a distribution of profit.

What are the Tax Obligations of NGOs?

1. NGOs must;

(a) be registered by the relevant law in Nigeria;

(b) not derive their profits or gains from activities of a commercial nature; and

(c) ensure that their profits or gains do not inure to the private benefit, that is, they must not distribute or share their profits or gains in any manner whatsoever with their members or promoters.

As rightly argued, the above is construed conjunctively hence, they are to be fulfilled altogether to warrant the exemption of an NGO from tax liabilities. See the cases of Rev. M. F. Shodipo v FBIR (1974) 1 NTC 273; Best Children International Schools Ltd. v FIRS (2018) LPELR-46727(CA).

2. Since it is only the NGOs that are exempted and not employees/ promoters, they are required, under the PAYE obligation, to deduct tax at source from salaries and other emoluments of employees, directors, officers, etc. and remit the same to the relevant tax authorities in the currency of payment of the emoluments.

3. It should be noted that the NGO itself is not exempt from VAT. As such, where the organisation procures contracts or purchases goods that are not directly used in humanitarian donor-funded projects, VAT shall apply at the prevailing rate. This also applies to services consumed by NGOs that are not exempted.

4. Under the CGT, gains from the disposal of chargeable assets of NGOs are liable to CGT where the gains are derived from the disposal of assets acquired in connection with any trade or business carried on by the institution or where the gains are not applied purely for the organisation.

5. By Section 55 of CITA, all NGOs must file tax returns every year and such returns shall include audited financial statements, tax and capital allowances computations and a formal statement containing the amounts of surplus from every source for the relevant tax years.

6. Registration with FIRS for listing under the Fifth Schedule to the CITA, for eligibility to receive tax-deductible donations under section 25 of the CITA.

7. Withholding tax: Whenever an NGO pays an organisation, individual or an unincorporated entity rent, royalty, management fees, consultancy fees, technical service fees, agency fees, supplies and contracts, appropriate withholding tax must be deducted and remitted to the relevant tax authority.

Conclusion

This work has been able to provide the basic information for the tax liabilities of NGOs in Nigeria. It argues that while NGOs are exempted from taxation under the tax laws in so far as they do not engage in business or trade, they are still required to register and file the relevant tax returns.

References

Vincent Okoukoni and Somtochi Onyiliofor, Nigeria: Finance Act 2020 – Public Character & Impact On The Taxation Of NGOs (26 May 2021) available from https://www.mondaq.com/nigeria/withholding-tax/1073068/finance-act-2020–public-character—impact-on-the-taxation-of-ngos. Accessed 2nd February 2023

B&I, Tax Treatment Of Non-Profit Entities In Nigeria, available from https://banwo-ighodalo.com/grey-matter/tax-treatment-of-non-profit-entities-in-nigeria. Accessed 2nd February 2023

Blue Print, Understanding NGOs and their tax obligations (Jun 2022) available from https://www.blueprint.ng/understanding-ngos-and-their-tax-obligations/. Accessed 2nd February 2023

Bicci Ali Tax Obligation of NGOs, (2021) available from https://www.thecable.ng/tax-obligation-of-non-profit-organisations/amp . Accessed 2nd February 2023

Finance Act, 2020

FIRS Guidelines On The Tax Treatment Of Non-governmental Organisations (NGOs)

Companies Income Tax Act (CITA) Cap. C21 LFN 2004 (as amended)

Personal Income Tax Act (PITA) Cap.P8 LFN 2004 (as amended)

Capital Gains Tax Act (CGTA) Cap. C1 LFN 2004 (as amended)

Value Added Tax (VAT) Act Cap.V1 LFN 2004 (as amended)

Company and Allied Matters Act, 2020

Requirements for Funds, Bodies, or Institutions for Listing Under the 5th Schedule to the Companies Income Tax Act, Cap. C21 LFN 2004” (the “Listing Requirements Notice”)

About the Author

Ater Solomon Vendaga is a Penultimate Law Undergraduate at the University of Abuja. He has keen interest in Taxation law, IP law, Technology Law and Public Policy.

****************************************************************************************

This work is published under the free legal awareness project of Sabi Law Foundation (www.SabiLaw.org) funded by the law firm of Bezaleel Chambers International (www.BezaleelChambers.com). The writer was not paid or charged any publishing fee. You too can support the legal awareness projects and programs of Sabi Law Foundation by donating to us. Donate here and get our unique appreciation certificate or memento.

DISCLAIMER:

This publication is not a piece of legal advice. The opinion expressed in this publication is that of the author(s) and not necessarily the opinion of our organisation, staff and partners.

PROJECTS:

🛒 Take short courses, get samples/precedents and learn your rights at www.SabiLaw.org

🎯 Publish your legal articles for FREE by sending to: [email protected]

🎁 Receive our free Daily Law Tips & other publications via our website and social media accounts or join our free whatsapp group: Daily Law Tips Group 6

KEEP IN TOUCH:

Get updates on all the free legal awareness projects of Sabi Law (#SabiLaw) and its partners, via:

YouTube: SabiLaw

Twitter: @Sabi_Law

Facebook page: SabiLaw

Instagram: @SabiLaw.org_

WhatsApp Group: Free Daily Law Tips Group 6

Telegram Group: Free Daily Law Tips Group

Facebook group: SabiLaw

Email: [email protected]

Website: www.SabiLaw.org

ABOUT US & OUR PARTNERS:

This publication is the initiative of the Sabi Law Foundation (www.SabiLaw.org) funded by the law firm of Bezaleel Chambers International (www.BezaleelChambers.com). Sabi Law Foundation is a Not-For-Profit and Non-Governmental Legal Awareness Organization based in Nigeria. It is the first of its kind and has been promoting free legal awareness since 2010.

DONATION & SPONSORSHIP:

As a registered not-for-profit and non-governmental organisation, Sabi Law Foundation relies on donations and sponsorships to promote free legal awareness across Nigeria and the world. With a vast followership across the globe, your donations will assist us to increase legal awareness, improve access to justice, reduce common legal disputes and crimes in Nigeria. Make your donations to us here or contact us for sponsorship and partnership, via: [email protected] or +234 903 913 1200.

**********************************************************************************